25 September 2025

Inflation Surprise: The RBA’s Balancing Act Continues

Inflation Hits One-Year High: What It Means for Borrowers

Recent data from the Australian Bureau of Statistics shows that inflation is again on the move: consumer prices increased 3.0 % year-on-year in August, up from 2.8 % in July, marking the strongest inflation rate in over a year.

This jump has significant implications — especially for borrowers, mortgage holders and anyone keeping a close eye on interest rate policy. But the outlook is mixed, and there are arguments on both sides of the debate. Below is a look at the key figures, what’s driving the rise, and what might come next.

Key Figures & Underlying Trends

In short: headline inflation is accelerating, but “core” inflation measures are diverging slightly — some softening, others pushing harder upward.Headline inflation rose to 3.0 %, but the trimmed-mean (core) inflation actually fell slightly to 2.6 %. That suggests not all price pressures are moving in the same direction.

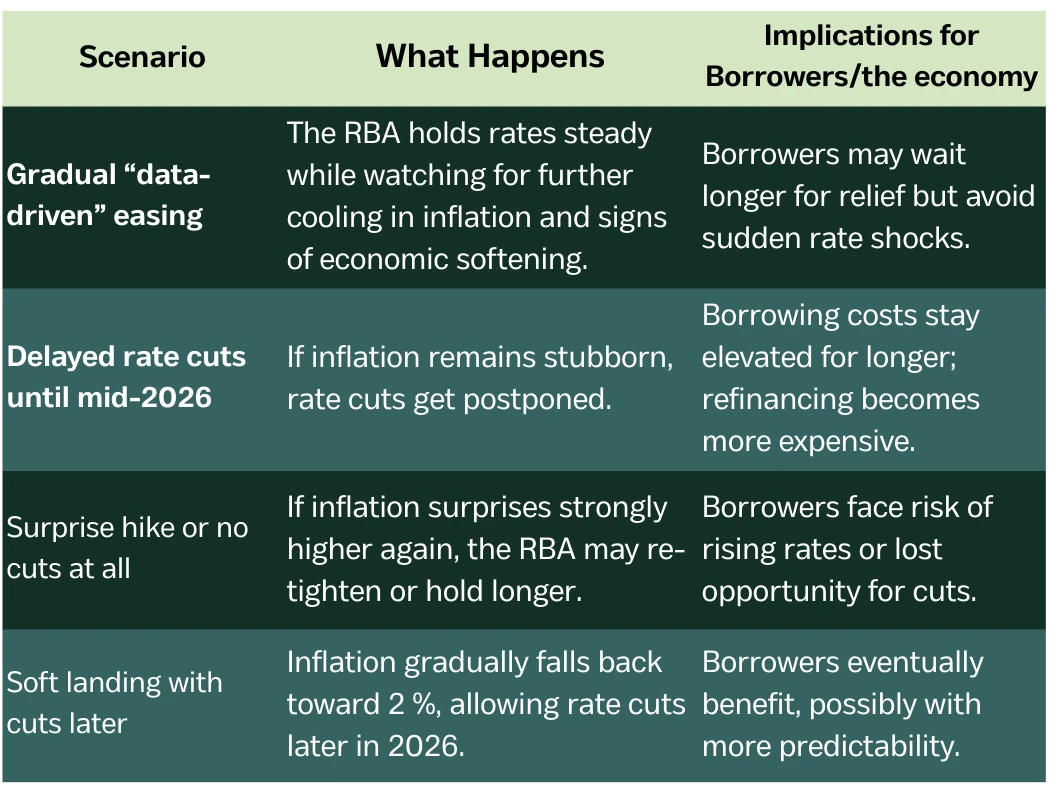

What This Means for Interest Rates & Borrowers

Arguments for a more cautious RBA

1. Volatility in monthly data

The RBA has historically cautioned against overreacting to monthly CPI prints, preferring to base decisions on quarterly averages and broader trends.

2. Softening core inflation

The slight decline in the trimmed-mean measure suggests that some inflationary pressure may be easing — possibly giving the RBA some room to pause.

3. Economic headwinds remain

If wage growth, labour markets or consumer spending soften — especially amid high borrowing costs — inflation could naturally moderate and reduce pressure for aggressive tightening.

4. Policy credibility & expectations

The RBA must balance inflation control with growth and avoid undermining confidence. Overreacting now could risk tipping the economy into stagnation.

Arguments pushing for “stay the course” or even tightening

1. Inflation is still rising

A rise to 3.0 % — especially above the top of the RBA’s usual 2–3 % band — adds urgency.

2. Underlying price pressures persist

The “ex-volatile” core inflation measure is rising, which may indicate inflation is spreading to more sectors beyond energy and housing.

3. Market expectations adjusting

Some major banks and institutions have already retracted or pushed back calls for an imminent rate cut.

4. Risk of inflation expectations becoming entrenched

If households and businesses start expecting higher inflation to persist, that can fuel further price and wage demands — making the RBA’s job harder.

For borrowers, these dynamics mean that interest rate risk is still very real. A pause in rate cuts may delay relief, while any further tightening would raise borrowing costs further. For those on variable-rate loans, the margin for surprise is higher.

What Borrowers Should Do Now

1. Review your loan structure — fixed vs variable interest components — and see if it still suits your risk tolerance.

2. Lock in where possible when market conditions allow, especially if you foresee further increases.

3. Build buffers in your budget — rising costs elsewhere could squeeze discretionary spending.

4. Stay informed — week-to-week data can be noisy, so watch quarterly trends, RBA commentary, and labour market updates.

Final Thoughts

The rise in inflation to a one-year high is a reminder that the fight against rising prices isn’t over. For borrowers, the road ahead may include a longer wait for rate relief — but with careful planning, there are ways to stay ahead of the curve.

Loan Studio Tip: If you’re unsure how inflation and interest rates could affect your repayments, reach out to our team for tailored advice.

Ready to take the next step?

Speak to a Loan Studio expert today and find the right loan for you.

Get Approved